Seth Walsh

Iconoclast

Contributor

- Joined

- Jan 12, 2020

- Posts

- 10,806

- Reputation

- 22,054

Okay guys. Increasing your social class isn't easy. But I will give you the inputs. What to do, what to avoid. How to think.

Eurocels needn't read this. Since tax, salaries, way of life and incentives differ so much from the States. I'll be making this primarily for US residents.

1/

Capitalism rewards four things: scarce skills, leverage, ownership, and trust.

Not effort alone.

Not credentials alone.

Not saving alone.

The move is: raise income, keep the spread, buy assets, enter better rooms, then scale.

2/

First: raise the price of your hour.

BLS 2024 data: high-school diploma workers earned median $930/week. Bachelor’s degree: $1,543/week. Master’s: $1,840/week. Professional degree: $2,363/week. Unemployment also fell from 4.2% for high-school diploma workers to 2.5% for bachelor’s workers.

3/

Do not “go to school.” Buy income power.

Simple test:

Annual income gain ÷ total cost

The bachelor’s-vs-high-school median weekly earnings gap is $613/week, about $31,876/year before tax. If a credential does not plausibly raise your income enough to repay the cost fast, it is consumption disguised as ambition.

4/

Aim at markets with high ceilings.

Good lanes: software, data, AI operations, cybersecurity, finance, sales, project management, management analysis, healthcare, construction management, skilled trades, and business services.

BLS lists multiple $100k+ paths with bachelor’s, technical, or apprenticeship routes: project management specialists, management analysts, financial/investment analysts, lawyers, computer hardware engineers, construction managers, sales managers, elevator installers, electrical engineers, and others.

www.bls.gov

www.bls.gov

5/

Job-hop only when the market pays you to.

April 2026 ADP data: job-stayers saw 4.4% annual pay growth; job-changers saw 6.6%. But Atlanta Fed’s April 2026 Wage Growth Tracker showed only 3.6% for stayers and 3.8% for switchers. Rule: switch for a better market, better title, better manager, better skill stack, or a clear comp jump.

6/

Income is step one. Ownership is the class ladder.

Fed Q3 2025 data: the top 1% owned 28.9% of total U.S. assets, the 90th–99th percentile owned 34.8%, and the bottom 50% owned 5.3%. You do not move class by spending every raise.

7/

Buy compounding machines.

NYU Stern historical return data: $100 invested in the S&P 500 with dividends at the start of 1928 became about $1,157,599 by the end of 2025. The same $100 in 3-month T-bills became about $2,578. Future returns are not guaranteed, but the lesson is clear: own productive assets for long periods.

8/

Asset order:

Fed SCF 2022: stock ownership was 58% overall, 95% for the top income decile, and 34% for the bottom half. Median stock holdings among stock-owning top-decile families were $608,000, versus $12,600 for the bottom half.

9/

Use housing as a balance-sheet tool, not an identity.

Fed SCF 2022: homeowners had median net worth of $396,200; renters/others had $10,400. But the same report says the median home was worth over 4.6x median family income, so buying badly can make you house-poor.

10/

The biggest jump is labor → ownership → scaled ownership.

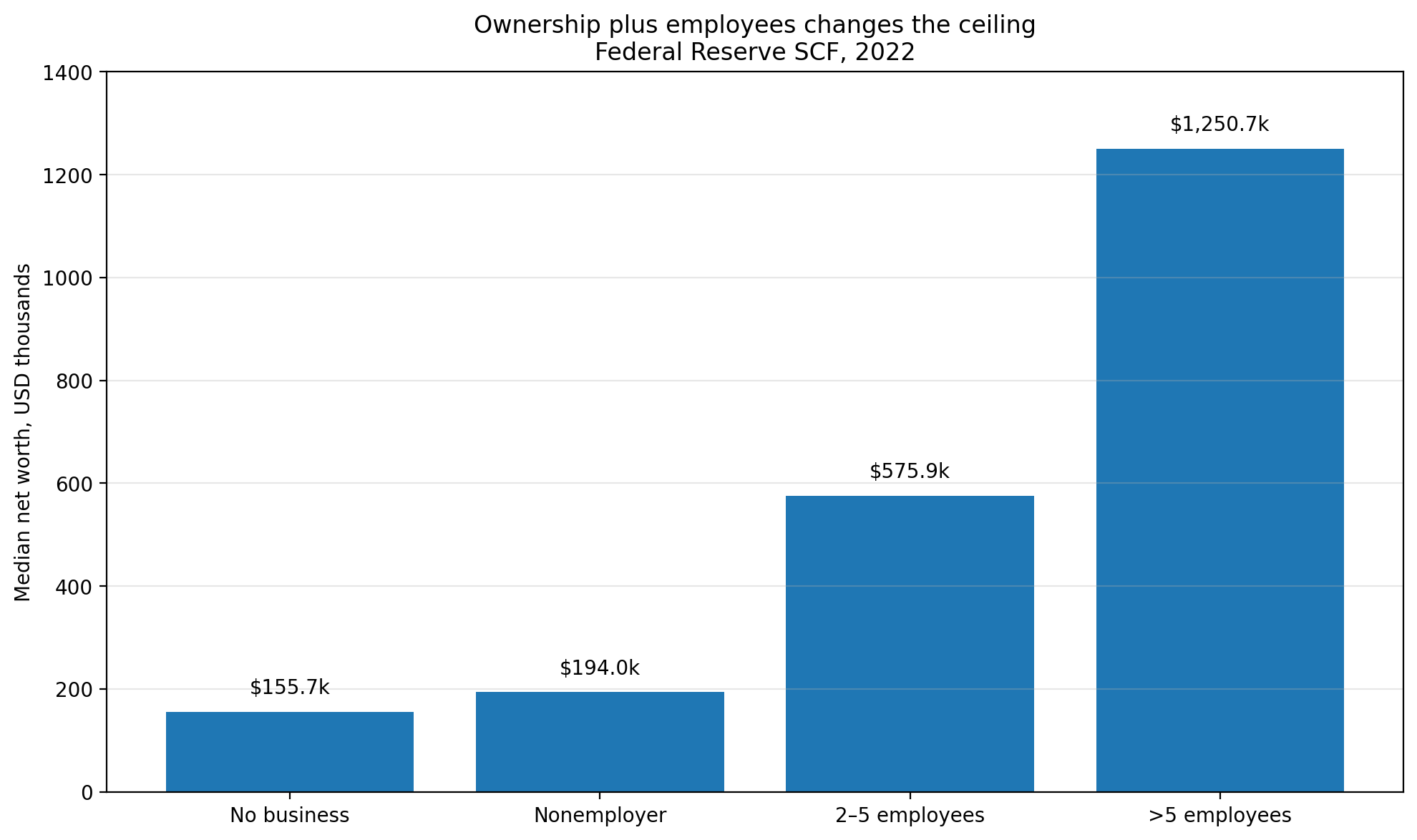

Fed SCF 2022: 20% of families owned a private business, and nearly half of top-income-decile families did. Families with businesses of more than 5 employees had median usual income of $237,200 and median net worth excluding the business of $1.25M. Families without a business: $67,000 median usual income and $155,700 median net worth.

11/

Move toward opportunity.

Opportunity Insights found bottom-to-top income mobility varied sharply by place: a child from the bottom income quintile had a 4.4% chance of reaching the top quintile in Charlotte versus 12.9% in San Jose. High-mobility areas correlated with better schools, more social capital, less segregation, less inequality, and greater family stability.

12/

Upgrade rooms.

Bad rooms normalize excuses, gossip, consumption, cynicism, and dead-end loyalty.

Good rooms normalize deals, hiring, ownership, discipline, fitness, capital, skill-building, and long time horizons.

Your network silently sets your default behavior.

13/

Avoid these traps:

14/

How to think:

30-day execution plan:

16/

12-month target:

Final rule:

If your life is labor + consumption, you stay in place.

If your life becomes skill + spread + assets + better rooms + leverage, you give yourself a real shot at class mobility.

Eurocels needn't read this. Since tax, salaries, way of life and incentives differ so much from the States. I'll be making this primarily for US residents.

1/

Capitalism rewards four things: scarce skills, leverage, ownership, and trust.

Not effort alone.

Not credentials alone.

Not saving alone.

The move is: raise income, keep the spread, buy assets, enter better rooms, then scale.

2/

First: raise the price of your hour.

BLS 2024 data: high-school diploma workers earned median $930/week. Bachelor’s degree: $1,543/week. Master’s: $1,840/week. Professional degree: $2,363/week. Unemployment also fell from 4.2% for high-school diploma workers to 2.5% for bachelor’s workers.

3/

Do not “go to school.” Buy income power.

Simple test:

Annual income gain ÷ total cost

The bachelor’s-vs-high-school median weekly earnings gap is $613/week, about $31,876/year before tax. If a credential does not plausibly raise your income enough to repay the cost fast, it is consumption disguised as ambition.

4/

Aim at markets with high ceilings.

Good lanes: software, data, AI operations, cybersecurity, finance, sales, project management, management analysis, healthcare, construction management, skilled trades, and business services.

BLS lists multiple $100k+ paths with bachelor’s, technical, or apprenticeship routes: project management specialists, management analysts, financial/investment analysts, lawyers, computer hardware engineers, construction managers, sales managers, elevator installers, electrical engineers, and others.

Occupation Finder

Search: Use the drop-down menu in one or more columns to narrow your search. Sort: Use the arrows at the top of each column to sort alphabetically or numerically.

www.bls.gov

5/

Job-hop only when the market pays you to.

April 2026 ADP data: job-stayers saw 4.4% annual pay growth; job-changers saw 6.6%. But Atlanta Fed’s April 2026 Wage Growth Tracker showed only 3.6% for stayers and 3.8% for switchers. Rule: switch for a better market, better title, better manager, better skill stack, or a clear comp jump.

6/

Income is step one. Ownership is the class ladder.

Fed Q3 2025 data: the top 1% owned 28.9% of total U.S. assets, the 90th–99th percentile owned 34.8%, and the bottom 50% owned 5.3%. You do not move class by spending every raise.

Q4 2025, Release Tables: Shares of Wealth by Wealth Percentile Groups | FRED | St. Louis Fed

Release Table for Q4 2025, Release Tables: Shares of Wealth by Wealth Percentile Groups. FRED: Download, graph, and track economic data.

fred.stlouisfed.org

7/

Buy compounding machines.

NYU Stern historical return data: $100 invested in the S&P 500 with dividends at the start of 1928 became about $1,157,599 by the end of 2025. The same $100 in 3-month T-bills became about $2,578. Future returns are not guaranteed, but the lesson is clear: own productive assets for long periods.

8/

Asset order:

- Emergency cash

- Kill high-interest debt

- Retirement/index funds

- Profitable side asset or business equity

- Real estate only when the payment does not trap you

- Concentrated bets only after your base is secure

Fed SCF 2022: stock ownership was 58% overall, 95% for the top income decile, and 34% for the bottom half. Median stock holdings among stock-owning top-decile families were $608,000, versus $12,600 for the bottom half.

Changes in U.S. Family Finances from 2019 to 2022

The Federal Reserve Board of Governors in Washington DC.

www.federalreserve.gov

9/

Use housing as a balance-sheet tool, not an identity.

Fed SCF 2022: homeowners had median net worth of $396,200; renters/others had $10,400. But the same report says the median home was worth over 4.6x median family income, so buying badly can make you house-poor.

Changes in U.S. Family Finances from 2019 to 2022

The Federal Reserve Board of Governors in Washington DC.

www.federalreserve.gov

10/

The biggest jump is labor → ownership → scaled ownership.

Fed SCF 2022: 20% of families owned a private business, and nearly half of top-income-decile families did. Families with businesses of more than 5 employees had median usual income of $237,200 and median net worth excluding the business of $1.25M. Families without a business: $67,000 median usual income and $155,700 median net worth.

11/

Move toward opportunity.

Opportunity Insights found bottom-to-top income mobility varied sharply by place: a child from the bottom income quintile had a 4.4% chance of reaching the top quintile in Charlotte versus 12.9% in San Jose. High-mobility areas correlated with better schools, more social capital, less segregation, less inequality, and greater family stability.

12/

Upgrade rooms.

Bad rooms normalize excuses, gossip, consumption, cynicism, and dead-end loyalty.

Good rooms normalize deals, hiring, ownership, discipline, fitness, capital, skill-building, and long time horizons.

Your network silently sets your default behavior.

13/

Avoid these traps:

| Trap | Why it kills mobility |

|---|---|

| Credit-card debt | Average credit-card APR was 21.00% in Feb 2026. That is anti-compounding. https://fred.stlouisfed.org/series/TERMCBCCALLNS |

| Lifestyle inflation | Every raise gets absorbed before it becomes ownership. |

| Low-ceiling loyalty | Staying loyal to a weak market is not virtue. It is underpricing yourself. |

| Status cars | They convert future capital into depreciating appearance. |

| Random investing | Concentration before competence is gambling. |

| Credential addiction | More school without income lift is expensive delay. |

| Cheap but isolated geography | Low cost means little if opportunity, mentors, and employers vanish. |

14/

How to think:

| Question | Meaning |

|---|---|

| “What is my hour worth?” | Skill price |

| “What % of income becomes assets?” | Ownership rate |

| “What debt compounds against me?” | Fragility |

| “Who sees my work?” | Network quality |

| “What scales without more hours?” | Leverage |

| “What room am I trying to enter?” | Class transition |

30-day execution plan:

| Day range | Action |

|---|---|

| Days 1–3 | List income, expenses, debt APRs, assets, skills. |

| Days 4–7 | Cut one major recurring cost. Kill or refinance highest-APR debt. |

| Days 8–14 | Pick one income skill and do 10 focused hours. |

| Days 15–21 | Apply to 20 higher-comp roles or pitch 20 higher-value clients. |

| Days 22–30 | Automate investing. Book 5 calls with people 2 levels above you. |

16/

12-month target:

- Raise income by 20%+

- Invest 15–30% of gross income

- Build one monetizable skill

- Build one asset: portfolio, client base, product, small business, or equity stake

- Move closer to better labor markets or better networks

- Remove one expensive status habit

- Track net worth monthly

Final rule:

If your life is labor + consumption, you stay in place.

If your life becomes skill + spread + assets + better rooms + leverage, you give yourself a real shot at class mobility.